To Stay and Grow or Cash Out and Go?

Most business owners view the sale of their business as the financial reward for their years of hard work and dedication to their passion. In many transactions, a business owner may want to keep a minority equity stake (for example, 10%-49% ownership retained post-transaction) in the business to participate in potential future growth and demonstrate to the buyer that they still have “skin in the game”. This retained equity stake is known as “rolled equity”. The ability to roll equity will likely vary by buyer type: strategic buyers generally prefer a full company buyout while an estimated 81% of private equity transactions [Goodwin Law] involve rollover equity from the seller.

What is a Majority Recapitalization?

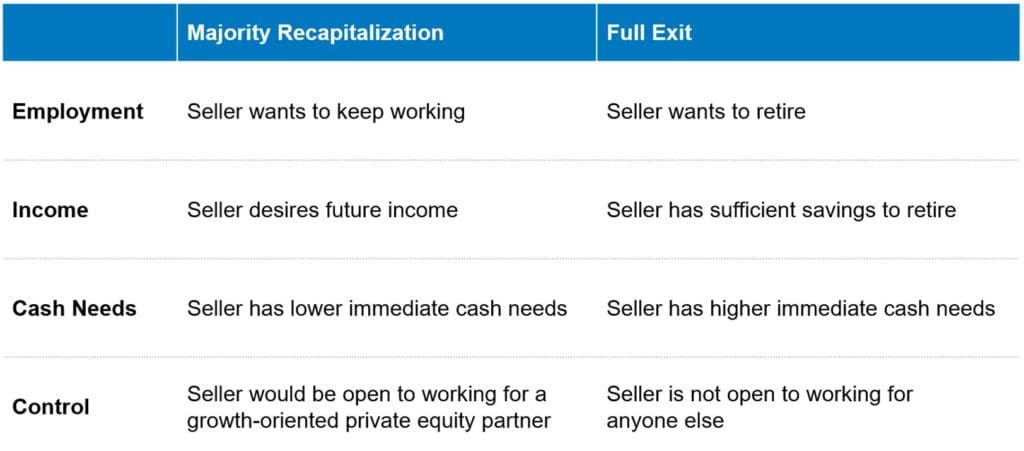

Rolled equity is also referred to as a majority recapitalization transaction, in which the owner sells a majority stake in the company to a buyer while retaining a minority ownership interest. This would be best suited for a seller who firmly believes in the future of the business and wants to participate in the growth of the company post-sale. (It is also common for an owner to retain a minority ownership interest while moving to a more passive role; this could entail a part-time consulting role, being a board member, or even eventually fully stepping away) The purpose of the transaction is to diversify the owner’s risk profile by taking chips off the table while still holding meaningful equity with significant upside in the business he or she has built. Though the decision is always based on the particular facts, the below is intended to help a seller think about what type of transaction they should be pursuing.

Private Equity Buyer Benefits of a Majority Recapitalization

Private equity firms like majority recaps for multiple reasons. The main is risk mitigation. In every transaction there is a varying degree of information asymmetry. While the buyer will perform due diligence and leave no stone unturned, the current owner’s tacit knowledge can be a concern. Rolling equity provides the buyer with confidence the seller believes in the future performance of the business and will be around long enough to transfer their expertise and relationships to ensure the success of the business following the transaction.

Private equity buyers will often see value in the management team in addition to the owner. If key members of the management team stay post-close and they had an ownership stake in the business pre-transaction, then having those key members hold some rollover equity aligns their interests with the private equity group by incentivizing their performance.

Seller Benefits of a Majority Recapitalization

A majority recap has its benefits for the buyer, but what about the seller? It is ultimately up to the business owner to contemplate their future financial goals and life plans best by weighing the pros and cons of rolling equity.

Often with founder-owned businesses, most of the seller’s wealth is tied up in their business. In an unpredictable business environment, the value of this wealth is subject to risks outside the business owner’s control. A majority recap allows the seller to take some “chips” off the table while still retaining the potential benefits of a minority ownership stake in the company.

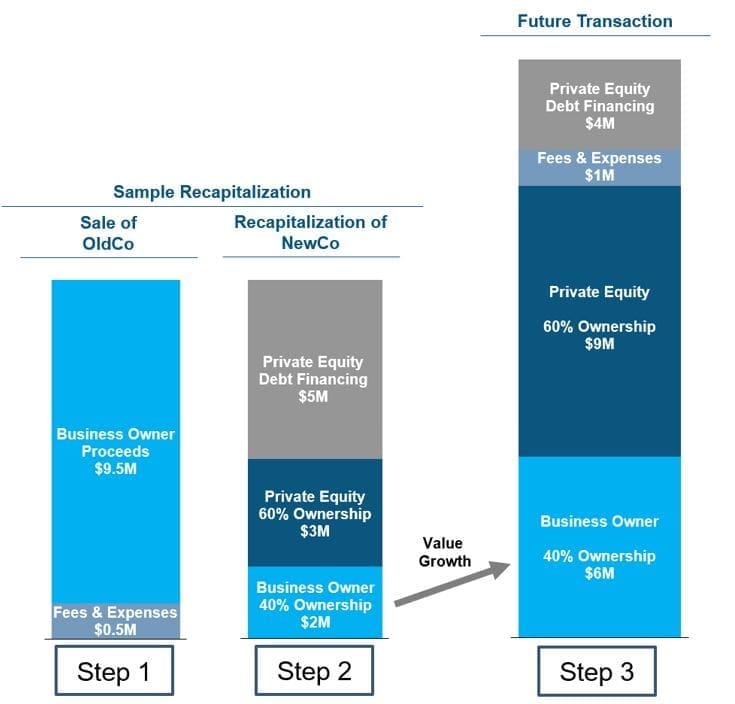

Although the seller will likely only retain 10% – 49% ownership, this has the potential to turn into significant future gains. Commonly referred to as the “second bite of the apple”, the seller should earn a second payout if the business is eventually sold in line with the buyer’s pro forma projections for the business, which is of course the goal of all private equity investments! The diagram below illustrates this type of transaction.

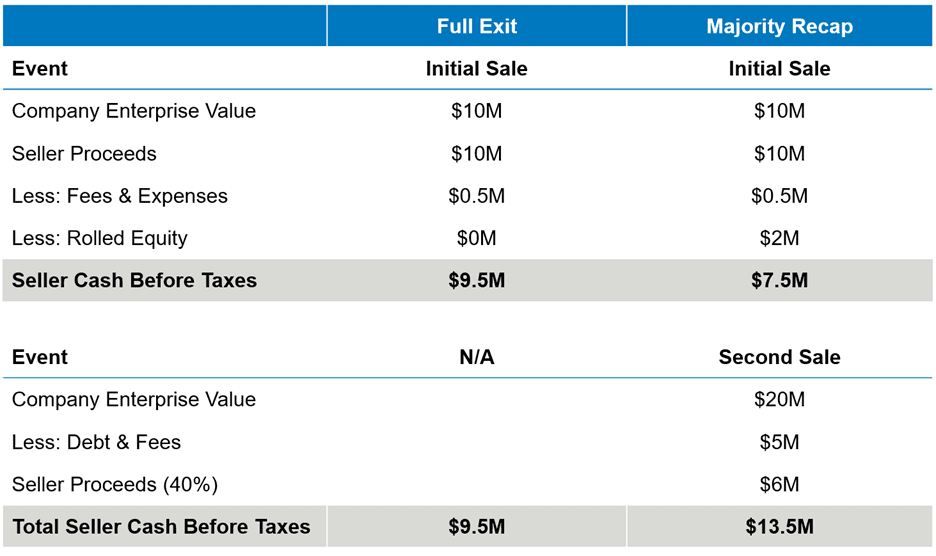

In this simplified scenario, the business owner is contemplating recapitalizing their company (“OldCo”) valued at $10 million with a private equity fund (Step 1). The private equity fund structures the transaction with $5 million of debt, $3 million of their own cash, and offers the owner an opportunity to roll $2 million of their $9.5 million cash proceeds net of fees and expenses as equity in the new entity (Step 2). As a result, the owner takes home $7.5 million cash pre-tax at the close of the transaction and retains $2 million of equity in the business.

60% of the newly capitalized business (“NewCo”) would be owned by the private equity fund with 40% retained by the seller. Assuming NewCo grows over time, it could double in value and sell for $20 million. The value of the aggregate equity of NewCo would increase from $5 million to $15 million and turn the business owner’s $2 million of rolled equity into $6 million, a 3x return (Step 3). As evidenced in the table below, when the business demonstrates growth and the seller rolls equity, the second bite may be almost as large as the first.

For owners who remain a part of the management team during the next phase of growth, rolling equity has additional advantages. Partnering with a private equity group provides access to more resources including capital for future expenditures, industry expertise, and potential synergies with other portfolio companies, among other resources to support future growth of the business.

Lastly, if structured properly, a majority recap can help lower or defer the seller’s tax bill. In most instances, only the cash proceeds of the sale would be fully taxable, thereby deferring taxes on the rollover portion of equity until the second sale of the company. Consulting professional advisors to ensure your equity roll is setup to be tax deferred is crucial to fully realizing the benefits of a rolled equity “play”.

Considerations for Rolling Equity

There are many variables a business owner should consider when deciding whether to roll equity. The questions listed below are important for business owners to contemplate in deciding whether or not to roll equity.

Personal:

- Do I want to take all my chips off the table now or participate in potential future upside that is not guaranteed?

- What are my immediate personal cash needs?

- Do I want to work for someone else? (this is not necessarily a requirement of rolling equity)

- If I continue working:

- How long will I be expected to remain with the business?

- How will my employment change? (salary, benefits, etc.)

- Do I trust the buyer to uphold the legacy of my business?

Financial:

- How will the rollover equity affect taxes? (will rollover be tax-deferred)

- What will the capital structure of the company look like and how will it change over time? (amount of debt, timing of payments)

- Will my equity be pari passu (on equal level) to the buyer’s capital?

- Does the buyer group charge any management or administrative fees?

Company Future:

- What is the direction of the company under new ownership? (culture, performance metrics / expectations)

- How will key strategic decisions be made?

- How involved will the buyer group be?

- What is the long-term plan of the new owners and do they have any experience with similar portfolio companies? (how much do you believe in their ability to execute their plan)

- Are there any references to contact, including managers of other portfolio companies?

- What is the expected timeline for an exit?

Conclusion

Rolling equity is not for everyone; each situation has unique dynamics that will determine the best course of action. While there are many questions to ask prospective buyers, the best place for a business owner to start is with their own desires and preferences. To avoid potential misunderstandings and mishaps, getting professional advice from an M&A advisor prior to engaging in further discussions with potential buyers is highly recommended. Nobody likes to eat rotten apples!