Multiples & The Market Approach to Valuation

A business’s value is generally based on the present value of expected future cash flows. Unfortunately, forecasting these cash flow streams can be difficult. The most common method of valuation, the Market Approach, derives a business’s value by looking at transactions for businesses within the same industry that are of similar size and operational characteristics. In theory, this is similar to how you might value your house, except that there are a lot more variables and comparable data is not readily available.

A key metric that is relied on with the market approach is normalized earnings before interest, taxes, depreciation, and amortization (EBITDA). This metric is used to approximate historical cash flow and was discussed in one of our previous articles. This article addresses how Enterprise Value/EBITDA multiples can be useful indicators of market value for privately held businesses.

Why are Multiples Used?

The EV/EBITDA multiple has been the primary metric used to evaluate M&A deals since investors began using it for leveraged buyout analysis in the 1980s. If not applied properly, EV/EBITDA could lead an owner to misunderstanding the value of their business. The appropriate multiple is predominantly a function of value creation, growth, and risk.

There are several reasons why multiples are used for valuing middle market businesses:

– They are easy to calculate and understand;

– It is easy to make comparisons to related companies; and

– Data may not be available to complete a more detailed valuation

A formal valuation may not be worth the cost and effort as they are complex, highly subjective, and may not produce a better answer than using multiples anyway.

Therefore, the key to valuing a small business lies in knowing how to determine and use an appropriate multiple.

Making Comparisons

The size of the multiple applied to a business for valuation purposes is rooted in the risk-weighted expected return on investment (ROI) of the business. Large, publicly-traded companies are generally less risky, more diverse, have experienced management teams, and are highly liquid. On the other hand, smaller privately-held businesses are riskier due to considerations like owner dependencies, inconsistent cash flows,and customer concentration. Generally, multiples are higher for lower risk public companies compared to smaller, riskier, privately held firms. Subsequently, the expected return on investment for public companies is higher.

To put this risk difference in perspective, the EV/EBITDA ratio for S&P 500 companies historically ranges from about 11-14x while most privately held businesses will usually have a multiple of about 4-8x.

Not every business is the same, so in order to make useful comparisons we need to be able to compare companies within the same industry that are of comparable size and operational characteristics. The challenge here is that most middle market transaction values are usually kept private. Fortunately, there are a variety of resources and databases to reference including: Done Deals, PitchBook, CapIQ, GF Data, and Pratt’s Stats.In fact, there are no less than 20 databases that compile deal details. Additional sources of transaction information can include other business owners, M&A advisors, attorneys, CPAs or other advisors who are involved in M&A deals.

For example, the table below summarizes 254 transactions in all industries from GF Data for 2018. This information is compiled from private equity acquisitions of privately held companies.

Source: GF Data

Of Note:

– EBITDA multiples (TEV/EBITDA) increase with the size of the business. The average EBITDA multiple is 5.6x for companies under $25M in value and 8.0x for companies between $100M and $250M.

– The EBITDA multiple for a specific company may deviate from the averages in the table depending on how the company stacks up in terms of size, growth rate over the past 12 months and EBITDA margin as a percent of revenue compared to the averages.

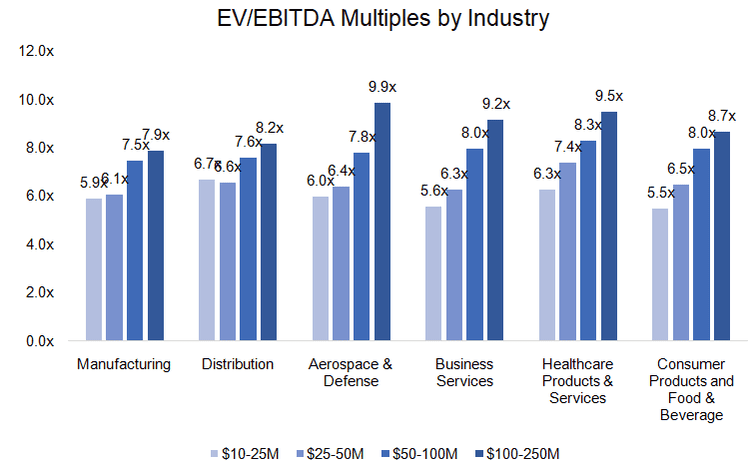

The graph below illustrates a selection of 1,198 transactions in all industries from 2014-18 in six select industries:

Source: GF Data, PitchBook

Considerations When Using an EBITDA Multiple

Although using EBITDA with an appropriate multiple is widely used for valuation, there are limitations. A common issue is unrealistic multiple expectations as a result of viewing comparable transactions, also known as “country club” multiples. Just because your friend sold their business for 7 times EBITDA doesn’t necessarily mean you will. Every business is different. There are other factors that cause valuations to fluctuate over time, including the overall health of the economy, interest rates, and buyer activity.

The market-based approach using an EBITDA multiple is a great starting point for determining enterprise value. It is important to understand the source and limitations of all researched information. Be realistic about your assumptions and don’t be afraid to validate them with feedback from others.

So, the next time someone asks you “What’s the multiple?” you can reply, “It depends.”