Introduction

For a founder, selling your business is one of the most important decisions you will ever make, and selecting the right buyer is key to taking care of your employees and protecting your legacy. Buyers differ significantly across the board and to ensure the right selection, it is valuable to understand the different types of buyers and the pros and cons that come with each.

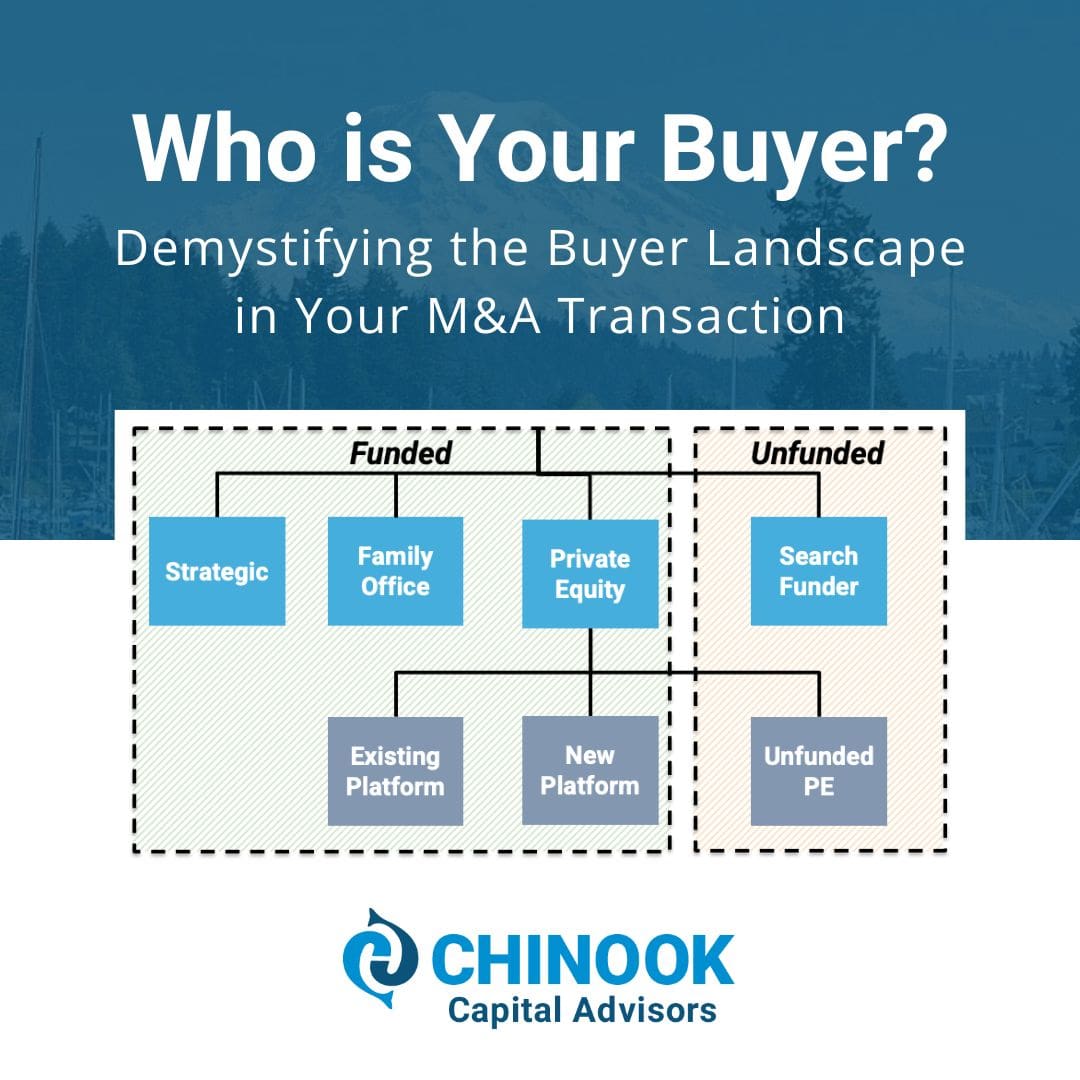

Strategic vs. Financial Buyers

Broadly speaking, there are two different types of buyers in an M&A transaction, strategic and financial. Strategic buyers are largely focused on utilizing M&A for operational improvements and growth into new regions, products, and services. Financial buyers execute M&A transactions to generate returns for investors, typically holding a company for a 3–7-year period. Financial buyers come with outside capital and can help accelerate growth through additional “add-on” acquisitions and other capital expenditures. In addition, financial buyers come with a wealth of knowledge in growing businesses and building the right management team to successfully transition your business when it is time to step away.

Buyer Types

Strategic Buyers

Strategic buyers acquire companies to further growth initiatives, expand into new markets, and solidify their position in existing markets. Strategic buyers can be beneficial in a sale due to having deep industry expertise and vast resources. These combine to help integrate and grow companies substantially by leveraging synergies between the two entities. Existing synergies provide strategic buyers with the ability to deliver premium valuations, leveraging customer relationships, vendor relationships, distribution channels, and other resources to create instant value when integrating similar companies. In addition, strategic buyers can often finance acquisitions using the resources on their balance sheet, oftentimes delivering 100% cash at close. On the other hand, strategic buyers have a predetermined business model and are more likely to make swift operational and cultural changes post-acquisition, which can substantially change the culture of your company. In some cases, PE-backed companies can act as a strategic buyer, say when their revenue exceeds $100m.

Financial Buyers come in a variety of forms, as follows:

Funded Private Equity

Funded private equity firms invest in companies out of a fund that has already been raised from institutional investors, such as pension funds, insurance companies, endowments, and family offices as well as high net worth individuals. Funded private equity firms are investing to return capital to their investors, looking to purchase, grow, and eventually sell companies after a 3-7 year hold period. By utilizing a mix of equity and debt, funded private equity firms can provide cash consideration upon closing, which is often coupled with rolled equity from the seller to maintain alignment with the PE firm throughout the investment horizon.

Private equity firms can generate outsized returns through the utilization of leverage and additional capital expenditures, but it is important to understand the risk profile before rolling equity. Although rolled equity provides sellers with the opportunity to realize additional growth throughout the investment horizon, continuing to invest in a company where you no longer have a controlling interest in presents risk and uncertainty that is not a consideration when compared to cash offers from strategic buyers. For more information about rolled equity, see our article “The ABCs of Rolling Equity: A Story of Chips and Apples” here.

Private equity firms also have unique operating styles that are crucial to understand as they ultimately dictate your life after the transaction. A hands-on private equity firm is highly involved in the business, assisting in operational decisions. This can be helpful for business owners looking for someone to guide them in successfully taking their company to the next level but can be challenging to work with at times if it feels like they are micromanaging the leadership team. Hands-off private equity firms take a much less prominent role in helping to manage your business, oftentimes only participating on a quarterly or annual basis, assisting with strategic planning, while leaving the day-to-day operations to the management team. This can be beneficial for business owners and management teams that want more flexibility in decision making but can be sub-optimal for business owners that are looking for guidance in growing their company over the investment horizon.

Unfunded Private Equity (also called Unfunded Sponsors)

Unfunded private equity firms operate the same as funded private equity firms but without committed capital. Unfunded private equity firms raise capital on a deal-by-deal basis, which can create additional uncertainty in closing a transaction as there are additional voices in the room that contribute to decision making outside of the PE firm itself. Even if the PE firm has a strong thesis and conviction about a certain deal, if they are not able to raise equity prior to close, the transaction will fail to go through, so signing an LOI and granting exclusivity to an unfunded buyer can be relatively more risky as compared to signing with a funded Private Equity firm.

Due to the added uncertainty of unfunded private equity firms, they are typically more flexible on deal terms as they need additional pull to win deals. This provides extra leverage for the sellers and their advisors to negotiate the best possible deal terms, including management incentive plans, tax treatment, and other key terms. Although the deal terms may be better for an unfunded sponsor, the uncertainty of close and general inability to compete with funded sponsors can be key factors for business owners when selecting a buyer.

Family Offices

Family offices are created to manage and invest the capital of one or multiple families, providing the family (or families) with the opportunity to diversify into different asset classes such as real estate and private equity. Family offices operate similarly to funded private equity firms but have longer investment horizons and a lighter touch when managing portfolio companies. Due to this, family offices generally do not pursue aggressive add-on acquisition strategies like private equity firms, and tend to pursue organic growth strategies over a longer investment horizon. Family offices prefer well-established leadership teams and are less likely to make operational changes in the business.

This approach provides founders and management teams with more breathing room to make operational decisions while under ownership, creating more independence to maintain company culture and direction. On the other hand, this approach creates a longer runway to liquidity, so for any seller that rolls equity with a family office, there may not be a clear pathway to final exit.

Search Funders

Search funders are generally entrepreneurs that have the goal of purchasing and operating a business. Search funders are often run by business school graduates and industry veterans that are looking to buy one single company and step in as the CEO. Search funders generally do not have the bountiful, fund-committed capital of a funded private equity firm or a family office, relying on bank debt and search funds, that approve transactions on a deal-by-deal basis, and oftentimes utilizing alternative considerations like seller notes and earnouts to minimize the capital investment at close. The sometimes-funky transaction structures utilized by search funders can create uncertainty in the deal process.

On the contrary, search funders provide founders with the ability to directly select the next leader of their organization, giving them the opportunity to evaluate not only their proposed operational direction of the company, but also their cultural and personal viewpoints. In practice, search funders self-source opportunities to avoid price competition. Overall, despite the personalization that search funders provide in selecting a buyer, the uncertain deal structures and general avoidance of price competitions restrict search funders from placing competitive offers and prevent them from winning auction processes.

Conclusion

Selecting the correct buyer is a key decision in the sale process, and navigating the different deal structures, financing methods, and risk levels associated with different types of buyers is complex. To ensure you can effectively evaluate these decisions, we recommend engaging an experienced investment banker to assure that each offer is explained thoroughly, the right questions are asked, and each consideration is effectively examined to ultimately select the right partner for the future of your company and to meet your goals.